The Canadian Tire Options MasterCard promotes itself as the best way to earn Canadian Tire Money on your purchases there and at other stores. You earn rewards everywhere you shop and earn bonuses for flyer deals. They advertise about %1 cash back.

- The first reason to avoid the Canadian Tire Options MasterCard is because the real rate is closer to %0.80 percent. They are intentionally misleading to make you think you get a better rate than you really do. This can really add up over the course of a year. For me it equals about $100 a year difference in the rewards.

- Secondly the website for this credit card is very vague, there are no details on the rewards. When you look at the gas card and cash advantage card there are much more details on the cards. On the gas card you save “up to” 10 cents per litre, this is also misleading because you only save 10 cents per litre for the first 30 days. After that you only save 2 cents per litre which you could easily save by going elsewhere to another gas bar. Additionally, here in BC there are practically no Canadian Tire gas stations. Normally one competing gas station will offer a gas price a few cents below the other anyways, so why not just go across the street to save 2 cents instead of signing up for a credit card with added baggage and hassles?

- The cash back card is even more misleading. How much cash back am I getting? It doesn’t say how much I’ll earn back it only says “up to 1.5%” and “up to 3% at Canadian Tire stores”. What is the real rate? The only way to find out for sure is to sign up, but really most people want to make the right decision with their credit card the first time. When I called in to ask about the details. I found out some interesting points that you should note.

- For the cash back card, purchases are always rounded down. A $235 purchase is rounded down to $200 and results in only a $2 reward.

- Also a $275 purchase is rounded down to $250 etc.

- Honesty. After our discussion they clearly knew the card would not amount to %1 cash back. All my purchases are rounded down to the nearest $50 it seems. Not very honest, I don’t think anyone would want to deal with a dishonest credit card company, especially if you have any issues down the road.

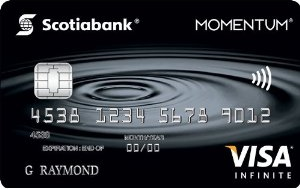

- There are better credit cards. For instance if your looking for a a better cash back card or low interest card, take a look at what Scotiabank offers, they have some very good cards that include no fees AND low interest rates, which is practically unheard of.

1. Scotiabank Momentum Visa Infinite Credit Card

Scotiabank Momentum Visa Infinite

| Type: | Visa |

| Rewards: | 4% cashback on gas, grocery 2% cashback on drugstores and recurring bill payments 1% cashback on everything else |

| Annual Fee: | $99 |

| Sign-up Bonus: | First year free |

| Redemption: | Full balance awarded automatically at the end of 12 month period |

Since this card is a Visa credit card, it will be accepted almost everywhere and it offers an extremely high cashback rate of %4 on gas and grocery spending. Not only that but for all other purchases it has a %2 cashback on spending at drugstores and for recurring bill payments. If you have large gas and grocery bills or use your credit card for bill payments this credit card would make sense for you to apply for. Many people forget or don’t get around to redeeming rewards so another great feature of this card is that the rewards are redeemed automatically at the end of each year. You won’t need to worry about not cashing in on all your rewards because of a redemption threshold. There is a small annual fee, however, given the huge rate of return this is my top pick for a cashback credit card in Canada.

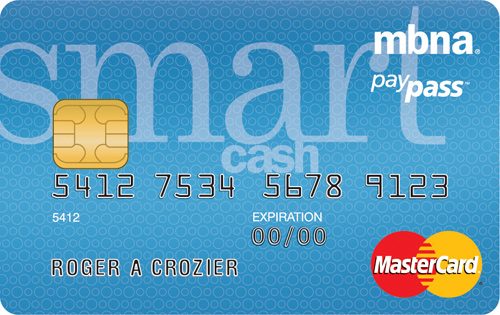

2. MBNA Smart Cash Mastercard

Click Here For The MBNA Smart Cash Review MBNA Smart Cash Mastercard

| Type: | Mastercard |

| Rewards: | 2 pt / dollar on gas, grocery 1 pt / dollar on everything else |

| Annual Fee: | $0 |

| Sign-up Bonus: | 5 pt / dollar on gas, grocery for the first 6 months |

| Redemption: | 5000 pt = $50 cheque mailed automatically |

The best alternative to the Scotiabank Momentum Visa Infinite to avoid the annual fee is the MBNA Smart Cash credit card. It’s very simple without the annual fee and offers a %2 cash back reward on gas and grocery spending. It’s a great offer for a no annual fee card and on top of this it offers a %1 cash back reward on all other spending, which is the standard for other credit cards. For this card the rewards will be automatically sent to you after you hit the threshold of $50 worth of rewards.

Take a look at my Google + Profile

i think that you should change the card you have pictured in our post, it is neither the cash back or the gas card offered by Canadian tire it is the rewards card that just saves you having to collect the Canadian tire money. The interest rate is only 6.99% not as much as 20.0% like many other cards. i for one like the card.

mike

The card pictured is not the card you are discussing; you have the Options Mastercard pictured. Anyone that shops at Canadian Tire wants the Options Mastercard, the reward rate is better than any other card I have had.

I have the options MC as pictured and the interest rate is 19.99%

Which one has the low rate?

good luck sucker. here is another reason to stay away from this card and this company. I had my card at 19.9% and was doing well they called & asked if I would like to purchase insurance in case of accident or job termination I said yes. but two years later when I was fired (without cause after 8.5 years).I continued to pay the card until E.I. ran out then applied for the insurance but because I had not applied within 30 days of termination I was disallowed coverage. Now that I am on O.W. and quite literally have no money the interest rate has skyrocketed to 25.99% and they have my son in law listed as an alias for me simply because I have had to move into a room in his home (thank God for loving kids) and are trying to make him and my daughter paymy bill. now I am pissed and am going to declare bankruptcy so they will get nothing! attack me for my mistakes great attack my kids and look out the repurcussions are on you!

My heart bleeds for people that are too stupid to read the terms and conditions.

Impossible. You sir are lying, you were not turned down for not applying with in 30 days of loss of employment. You’re talking about credit protector and I know the product under written by the American bankers association. And u can back claim as far back as you had the insurance. I work for assurant solutions and I’ve processed claims as far back as 5 years because they didn’t know they had that insurance. If u got declined then u didn’t meet the criteria and u don’t want to admit it. So u were probably fired and now ur taking out your anger on ct…. Real mature for a guy who lives with his adult children

I have had the Options for 12 years, best rewards compared to my other cards. No fees and with good credit I have a 10.99%. Don’t usually carry a balance but you never know.

I personally love my CT card using it exclusively. I have two MBNA cards and have had bad experiences with them (MBNA).

They say you get 1% back. But you have to spend that at canadian tire. So, if you saved up $50 in canadian tire money and bought an article worth $100. Your bill should be $50 plus the %13 taxes which would equal $56.50. No Canadian tire charges you the taxes on the $100 purchase which puts you at $113 dollars owed and then takes the $50 dollars off which leaves you with having to pay $63 in the end. That is $6.50 more than you should be paying. Where is this money going. It shows that the 1 or 2 percent that you think you are getting isn’t actually right. You are getting scammed. I’m switching my credit card to a true rewards card.

That is incorrect math. You are not getting a $50 discount on the item you are buying, but are simply getting $50 in Canadian Tire money. Rightly so that 13% tax is charged on the full amount before applying any deductions of Canadian tire money.

That is correct.

And just an FYI, the government requires it to be worked that way. Take a guess why.

Go complain to them. It’s not CT’s fault. They’re just little fish in a shark tank like the rest of us.

Canadian Tire MasterCard is THE worst credit card around. I pay my bill in full and they are always trying to tack on hidden fees. Customer service reps are rude and extremely confrontational. Not worth your time

You’re full of it. They do not “tack on hidden fees”. Pay your bill in full each month, and there won’t be any interest. Don’t exceed your credit limit, and there won’t be any over limit fees. Don’t take out cash advances, and there won’t be any fees for that. You and I, and everyone else reading your post, knows exactly this is the “hidden fees” you’re referring to. I got my Options card in July 2013 with a $3500 limit. Called CT to inquire about something in January, and was offered a pre-approved $5000 limit with no credit check. Now today, they offered me the upgrade to the Options World Mastercard, that has a better reward rate, extended warranty, and other features the regular Options card doesn’t have. You can’t apply for the World version of this card, it’s an invite only card. I use my CT card for almost everything, and rack up anywhere from 30-60 transactions every month. I pay my bill in full, and have never paid a cent of interest. You do the same, and CT will treat you as a good customer and start throwing offers your way. Then you won’t have to worry about writing these bogus complaints about the CT card.

Well, I have worked my wayl up to a 10K credit limit (after several increases proposed to me over the years since 2005). However, lately, the card stopped working in stores (the chip must have stopped working). I called to get a replacement card, which was done without any problem. However, a few days later (on the first of the month), my credit limit was reduced to 6K. I have not received any notice yet, I just saw that online. Or, I’m not just a good payer, I pay better than well. I am normally paying my balance before it is even due and starting the next billing cycle with a 0 balance. At this time, I only owe about 300. The usual balance that I would reduce to zero tends to be over 1k but below 2k, although once or twice it was over 2k and my credit limit was not affected. This very month, I have already paid back the exact amount of a large-ish purchase (almost 800) precisely because I’m trying to keep the next payment within the usual limits (I should be fine). Instead of being rewarded (or left alone) since I’m paying so well, I got my credit limit cut behind my back. On the other hand, a long time ago, I used to owe money and I got rewarded with a credit increase as soon as I made a large payment. Go figure! I’m getting penalized for paying quite well while I got rewarded for being less responsible and able to pay.

This is a MasterCard policy not ctfs. Every MasterCard has a 0% fraud liability. So if ur card gets defrauded MasterCard pays for it not you. So if u don’t get anywhere near your limit for a long time MasterCard will reduce your limit to minimize their exposure… It’s really not ct’s fault they can’t control it

,well I have had the options card for 12 years and use it for everything as you pay my bill totally at the end of month and have never paid interest. Never had any problem with this company, the interest that I would pay if I was to carry a balance is 10%,i would recommend this card to anyone.Thankx….

Well said, Wayne. I use my Canadian Tire Options MasterCard exclusively, for absolutely everything and love seeing the Canadian Tire Money rack up. I have found that if you’re good with credit cards, they’re good back to you. I keep about $1500-$2000 dollars on the card, so that CT always owes ME, and have never paid a single cent of interest since I got the card around 5 years ago. I just got an invitation to join the World card, and will likely be jumping on board.

just got limit increase on my ct option MasterCard, just a question can I use it any where or just Canadian tire??? I’ve been using it for over a year at Canadian tire and I always pay before interest charge that’s why I got increase I guess ..

It is a Mastecard so you can use it anywhere Mastercard is accepted.

Thanks.

i never noticed any hidden fees and never had rude cs

I just applied for mc @ the store. I was approved then and when I received card in the mail, I called to activate and the told me, `this account has been closed and the don`t know why`. This is my first mc. I have been working over 2yrs all information was accurate. I cannot understand why the account was closed. I will never apply for this mc again.

Canadian Tire financial are the most ignorant of all credit card companies to deal with, I paid mine down then off and will never use their services again. If you ay of credit cards monthly and don’t hold balances you ca choice what shit you are willingly to take.

How did you get signed up for yours Tom? In store or during a promotion?

My experiences with CT Mastercard have been nothing short of great.

I applied for this card not even 2 years after being discharged from bankruptcy (and having 2 secured cards since my discharge). I was in utter shock when I got a card with a $2K limit in the mail (instead of a rejection letter).

Needless to say, I cancelled my secured cards right away.

The customer service has always been great. Not a single bad experience.

I started out with the base version with a $2K limit, and I’ve since worked my way up to the World version (the black one) with $10K.

The interest rate? 16.99%. Quite reasonable for what it is. Then again, I usually pay in full every month.

I could care less about the rewards.

Liam,

I have the exact same story. Someone approached me one the store and I never thought I’d qualify after bankruptcy. I had zero credit for anything, then boom, a 2K card appeared in the mail.

10 years later I have the Black World card with a 18K limit, and like you, a 16.99% interest rate.

Gotta appreciate them giving me a chance 🙂

After 40 months of having it, I got upped to $17,000.

Not to mention, my card recently got compromised, and the whole situation was handled VERY well.

I also recently managed to get a Desjardins Visa with a 6K limit and with a rate of 9.9%

CT isn’t THAT bad after all 🙂

Most of these forums simply don’t take in to account that not everyone has perfect credit.

Good ole Scotia has to screw you for 7 years after bankruptcy – as do almost all banks. TD requires you to be discharged for at least 3 years before even being able to qualify for a secured card, and even then you might not get it.

Oddly enough, when I called to cancel my Capital One secured card, the lady even said that they lose a lot of business to Canadian Tire.

Compare CT to what’s available to those in the US with subprime credit, and this looks like a Centurion card compared to those.

The best part by far is the service. You don’t get someone in India or the Philippines – you get someone in Ontario, which is the way it should be. Sure, there might be the odd bad apple (as some people have mentioned), but there are bad apples everywhere.

When you call Amex, HSBC, Capital One et al, you often get India or the Philippines. I once found someone’s US HSBC Premier card, and when I called the number on the back I got the Philippines. I found it strange that high valued clients would have their calls answered in the Philippines!

Don’t get me started on the h*** I went through applying for a US-based Amex card and dealing with their credit department in India. YIKES! I got it eventually, but it required me to go all the way to Niagara Falls, NY twice to get a letter from Social Security stating I don’t have a SSN. I had to go a second time because the letter got “lost” by Amex despite paying for tracking, and then an excuse stating that it wasn’t lost, but rather that it wasn’t what they were looking for, and thus another trip and I eventually got it.

CT will always have me as a customer since they’ve been the best overall.

With 28 years experience using credit cards, the Canadian Tire Options Mastercard is beyond question the BEST credit card I have ever owned. I use it for absolutely everything and charge about $60 – $70 K per year on the card. I have no idea what the interest rate is because I pay the balance in full every month (current balance is about $7,200.00). The card has a $20,000 limit and earns EXACTLY 1.5% on all purchases. I earned over $900 in Canadian Tire money last year and can redeem it at anytime with absolutely no hassle. Additionally, once or twice a year I have had a fraudulent expense charged to the card. When I call or email to clear up the situation, the charges are removed instantly with no questions asked. Absolutely no hassles.

I was approached about two weeks ago at a Canadian Tire gas bar, and when I was about to pump gas I was given a very assertive sales talk by one of their salespeople. He told me I would get ten cents a litre off my purchase, and made it appear as if all I had to do was apply. I had to give him my driver’s license and answer a few questions. I told him that I probably wouldn’t be approved (I have slow payments on my file, from when I was surviving off tardy WSIB payments) and he said don’t worry, I’ve seen approvals for people that have been going thru bankrupcy. Of course, I didn’t get approved – nor rejected immediately either – and it turned out that the discount was only for people that are approved on the spot. About a week later, I received my (polite) letter telling me that they couldn’t offer me a card right now but to re-apply in six months. Fair enough. Now, a few days after getting that letter, I’ve been receiving collection calls on my cell, from a company that buys old or paid off debts (according to my research anyway). I am so p*ssed that I gave them any of my information. I feel that they didn’t really care about promoting their product, but use these applications as a method to troll for personal identification they can then turn around and sell to unscrupulous companies. Never again will I fill out one of these stupid cards!

I am so sorry you went through this. This is a good story for others interested in applying for this card.

Yeah, that’s not really how it works. When you apply for credit, your bureau information is updated with information you provided when applying for credit. If another company to who you own a debt accesses that data, then they are entitled to do so in order to collect. Canadian Tire didn’t ‘Sell your info’ to other companies. They merely updated your bureau (as is required by law) and probably another company did an inquiry. This is how the credit system works. I’m sure if you read their privacy policy, you’ll find they don’t sell any information retrieved via applications.

The marketing team (3rd party, don’t work for CT) at the stores and gas bars are kind of annoying. They frequently don’t give people all the details or don’t explain things fully. It’s amazing how many people will give all their personal information so someone and not clue in that they’re applying for a credit card (despite signing the application). I’m not saying that’s your story, sounds like you knew it was a CC, but people shouldn’t be surprised when they apply for a credit card, and the things that happen when you apply for a credit card happen.

Far too many trolls on this post. Most of the poor experiences can be explained away by poor personal finance practices. CT DO reduce credit card limits (as do most CC companies). But only if you are not using the limit. If you use, say $2000 a month, whats the point in giving you $10,000. If you know you will require it, just call them.

“Tacking on fees”. Load of garbage. No CC company does this. Read the fine print and you will see every fee they can charge.

Gas Card – 10 cents per litre. Read the fine print again. If you sign up at a gas bar event, you will get 10 cents for 30 days. It doesn’t then revert to 2 cents automatically. It reverts to a level depending on your spending the previous month. $0-$499.99 = 2 cents, $500-$999.99 = 5 cents, $1000-$1999.99 = 8 cents, over $2000 = 10 cents. Each month it is reviewed and changes accordingly. And, don’t forget, if you are approached at a gas bar event, you have called in because you want the 5 cents/litre saving they are offering that day. There is no such thing as a free lunch! Why do you think they offer that deal if not to attract new customers.

Some people really need to understand their CC terms. If they don’t, then they shouldn’t have a CC.

And, BTW, the interest rates in Canada are disgraceful. In the UK, they used to fight over signing up customers with offers of 0.9% APR for 6 months. If you carried a balance, you would just credit card hop as the offer expired.

what you and most people dont realize is that not everyone has perfect credit through their own fault or not. therefore they dont have the luxury of picking and choosing cards that offer lower interest rates and better reward programs. They simply must take the card that accepts their application. My Canadain Tire Options Mastercard has been fantastic and a blessing for me. Could it be better sure it could but it does the job and they also gave me a chance when the snob nosed banks spit on you. Have a great day

Thanks for the comment. I think this can serve as a nice data point that the Canadian Tire Mastercard tends to be more approving of a lower credit profile.

That being said, my understanding is that there are better offers for people who are carrying a balance or if you have lower credit profiles. Those might be better for you. However, there are people who this Canadian Tire Mastercard are for. You might be this exact market that is perfect for the Canadian Tire Mastercard. IF you have found each other, then I am happy for you.

In our analysis, we have found that there are better options for the majority of people who might be interested in either a better rewrads program or a lower interest rate.

I have my CT card for about 14 years now. With $18,000 limit and 6.99% rate, its pretty hard to beat. We spend about $2000 a month and paid off full every month. Never had issues or extra fees added. The rates are offered by CT by invitation only. I shop at CT regularly, so it just makes sense to have their card. There are other cards out there that offer the same or better rewards, that’s why I have other cards also for travel/car rentals.

Do not sign up for this card. They are very rude and confrontational. They called my wife when I lost my job and stated that if the balance was not paid in full I would take a credit hit even though I arranged payment plans when I lost my job. It is simply the worst card I have ever had and will most defiantly not recommend anybody to get one. Like others have said there are better cards out there, and I guess it boils down to paying the card in full every cycle. Even if something bad happens they won’t really work with you they only care about making their money off of you. My card is now paid in full and the account is closed. I will never again apply for this type of card. Worst experience ever.

If you value excellent customer service where you at least expect to be respected as a customer, then do not waste time with this card. I phoned their customer service today for the second time in two months informing them that I wanted to pay my account but could not because I have not received any statement, I was told that my statement was returned due to an invalid or wrong address. When she verified the address with me, there was nothing wrong with it so I countered why the letter would have been returned. The response was a rude “why don’t you phone your mailman” – just the kind of response to lose a business. This card will be off my wallet now.

I really like to read your website, fortunate for me to found this mavolous blog. This content provide informative data to us, keep it up.

I strongly recommend to people not to sign up with Canadian Tire MasterCard options. When you first register they

tell you you have 10 dollars free, it turned out that money is a Canadian Tire money it has no value and you find yourself with a balance due to pay plus interest. That money is worthless DON’T SIGN UP.there are traps.

I am working on a story about a gentleman who attempted to use his CT card at a gas bar in Detroit. The machine would not accept a Canadian card, and Canadian Tire had never advised its cardholders, in writing, as required by law, of a work-around to this problem, which has subsequently been promoted by MasterCard itself on its own Facebook page. They KNEW there was a problem, but never advised anyone.

The fellow whose story I am telling had to go in to the store, but never made it in there before he was accosted, robbed, and injured. Canadian Tire knowingly let him down, as other banks had advised in writing to their cardholders to enter the “00” after the 3 digits in the postal code, i.e. M1P 2R7 = 12700. Canadian Tire has been acting like a sanctimonius bully, telling him to basically get lost, and wishing that he had died in the confrontation. They COULD have done something without admitting any liability by making a donation to a humanitarian organization that he founded to help overcome his depression and anxiety…no, they keep harassing him for payments on his CT cards, knowing full well that he was injured (in no small part because of their card!) and is awaiting insurance settlements! Shameful hypocrisy. Canada’s Store, don’t go to the US with our card should be their tagline. This is NOT the Canadian Tire that I grew up.

Over the last couple years I have been trying to re build my credit. I have a secured card with Capitol one now that is $1 over the limit but my bill is not due yet. I have a great job that pays well and my only debt is a car loan. I recently went for a mortgage and the broker said my score is a little low (just below 600) because I missed a credit card payment in May. He advised me to apply for a CT credit card and pay off my $300 Capitol one card and said this would help get my score up. I’m a little worried about getting declined for having a missed payment in May, resulting in another ding on my credit report. Are these cards easy to get approved for, or am I basically further sabotaging my score?

I close my account and realized I have a credit (overpaid) of $235 from canadian tire options mastercard. I called them twice already about my credit. They told me they are going to send the cheque to me within couple of days. Almost two months now, I still have not gotten my cheque yet.. :(:(:( … What do I have to do now?? Sue them??

YOu can call them and ask them and if that doesnt work call Ombudsman of Financial Affairs.

I have had the Options MasterCard for 4 years. I did not have good credit and they issued my card without hassle. $2500 Credit Limit @ 25.99%. Gradually I moved up to a 13k limit but still only @ 19.99%. They would not budge on the interest despite other banks offering me better rates.

When I changed my name it was nothing short of a HUGE hassle to deal with them.

I recently received a 0% balance transfer offer with 3% transfer fee. Sure enough, Canadian Tire found a way to tack on the hidden fees and charge me interest. I called their customer service and was hung up on; I called once again and the Representative blamed the telephone and also did nothing to really help resolve the issue. Sure enough I told them that I would be closing my account.

If you have poor credit this card will help you rebuild it but once your credit is repaired I would steer clear of this MasterCard!

I was recently encouraged to take out a Canadian Tire credit card by a young lady ( im 71) and on

Y agreed after she said let us send an application to your home. I relented if only to continue standing and waiting at the front of the store.

She asked for my address and then iMO feigned she couldnt hear and asked for my drivers license to copy it correctly.

Instead of sending me an application in the mail she printed off the details in a long cash register tape . And said they would send the card to my home.

Too late i realized id been scammed and they had not only checked my credit rating but issued another card both of which would result in a reduction in my credit score. Since this personally effects my rate for an upcoming mortgage renewal i am considering suing for damages.

Your stories about giving breaks to new or poor credit risks concerns me. Car insurance rates are determined by credit scores more than any other factor. I suspect having a canadian tire credit card,might work against you i e personal auto repairs.

Are there any other personal financial and or credit consequences to this. i should consider? As i have for the first time started to receive robo call phone calls from 800 numbers on My US based voip service. I use it because it is totally free of telemarkreting calls.

Will Canada tire phone numbers suddenly appear on telemarketets lists,.its been 3 years since i had a call.

I was able to get the employment history of this marketer .

Would you suggest a boycott. And no i have not used the card and have no intention of using it.

The Options MasterCard earns e-Canadian Tire Money. If you buy gas at Canadian Tire, make a few purchases at Canadian Tire stores and use the Options MasterCard for daily purchase outside Canadian Tire, e-Canadian Tire Money really adds up quickly. One of the things I like best about e-Canadian Tire money is that Canadian Tire treats it like real money so it even covers the tax. I can turn the e-money into tax-free items anytime I want, and for items I was going to buy anyway. The card does not have any fee and if you pay the balance if full every month it doesn’t matter what the interest rate because you won’t pay interest.

Few things I want to say about Options MC that I have for 7 years now.

– I never paid attention to reward calculation, so no comment there. Seems lower than their ad claim. Misleading on website re: 10c per litre, when you go in fineprints & actual gas saving is only 2c per litre. So, I decided to not get the gasadvantage card.

– I still have the Options card, Downside is that you can only spend it at canadiantire store. Yes, the taxes first and then deductions … will add 6.50 as per SJC’s point earlier. Sales tax is collected on behalf of CRA, and Organization is responsible to submit a return at the year end.

While HBC would apply discounts first, then add taxes on real payment… because that is what corporation submits to CRA in your corporate tax return [on actual sale/transaction amount, not list/’before discount’ sale amount — whatever their tax return method is, quick or detailed]. SO, yes that is another rip-off. They keep extra in their pocket.

– yes, credit card limit (both higher & lower) & interest rate changed without notice. Just found out after login as Monica said.

– I am still using the card anyway. Evenif it is less than 1% return, it is something- better than nothing. Everyone shops at canadiantire, feels nice to get some rewards once in a while.

Thanks !!

I forgot to mention – they never email notification before/after they issued electronic statement.

but for sure, an email notification “Oh, you forgot to make the payment, now pay interest”

I do not know what happened to the “electronic statement notification” like all other banks & credit card companies.

i agree that they did misrepresent the percentage you get back, i did not like that either

but ive been told since then they have changed

its a higher percentage and thet dont round anymore

the few times i actually check, it seems correct

My wife and I have used this card for years. Never had any concerns. Always had fantastic customer service. Just paid the card off and was offered a credit increase!! Rewards points are a bit falsely represented but I don’t use the card just for the points system! No issues using the card anywhere in Canada!!

it is the worse company i have ever dealt with they give you the cc even before the decision is made and you call their customer care they talk as if they don’t care at all.until i reached the last one.worse experience even before start.

This is the worst company i have ever ever applied to never ever going back to them and warn my friends not to.

EXTREMELY DODGY CORPORATE CUSTOMER SERVICE BEHAVIOUR, not from the customer service reps, but the company itself.

Its true what others are saying about cancelling cards without telling you or giving an explanation.

So I did my tour of duty at school, was paying back some loans when the NBNA harassment started for me to get their card. I looked online and saw some of their practices at the time and ignored their mail.

Then I got approached at a CDN Tire store when the Options card I guess was still pretty new at the time. I was shocked, as I never thought the credit check would go through.

I had the card for over 5 years and went back to school and wasn’t using that much, as I got approached for a PC Master Card,. Options lowered the rate significantly, around 14% but I was in school and still wasn’t using it that much. (I have learned my lesson)

Without telling me these idiots completely cancelled the card. I think they had sent me a letter a year earlier to use it more, but they never said it will be cancelled.

I doubt they sent another letter as I’m good with financial matters and keep up with my accounts. Well it was exam time and I didn’t have time to track down the issue, as i hadn’t received a statement in a while. But I didnt have hours to spend on the phone.

When my exams was over, I tried contacting them, even the managers COULD NOT FIND AN ACCOUNT WITH MY NAME ON IT. they didn’t even have me as ever being a customer OR EVER HAVING AN ACCOUNT.

THEY TOTALLY CANCELLED THE CARD WITHOUT WARNING OR TELLING ME. Is this they way a REAL financial institution operates? Shocking if you ask me

Isn’t that perverted?

Applied for CT MasterCard in store and received in the mail. After activating and using it 6 times I try to pay for a dinner worth a little more than $120 and transaction declined. Phoned customer service up and tell me they want to call my employer to verify my job!?! Probably the most asinine reason I’ve ever heard of a bank cutting off a card and quite embarrassing for me actually.

Will be closing this account and dealing with an institution that doesn’t find lame reasons to humiliate customers. In truth the card products are just as crappy as the Canadian Tire stores themselves. Stay away is my advice.

Here’s a real story – 6 months ago my wife loses her job immediately after we purchased our first house and first new car. Our first house was not new, so needed some additional work, which we had taken out a loan to pay for…then BAM she’s unemployed and our bills are more than one income can handle. Before we get into trouble financially, one call I make is to CTFS (had been a customer for almost 1.5 years). I request my card to be cancelled (as it was the highest interest rate of all our cards), and when asked why, I simply said that we were making financial changes to reflect our current position – I was dumb founded when CTFS asked me not to cancel the card, as I was a customer in good standing, and me offered 6 months with 0%…which I was grateful to accept. 6 months later however is when the bomb dropped…after not missing any payments, and after get a handle on things, I had the money to pay off my balance, which I do. I then get a call from CTFS thanking me for paying off the balance and asking if i’d like the ‘hold’ removed from my card (what hold?) – apparently a hold was put on my account because i was a person listed as ‘in financial trouble’, and to have the hold removed, they ‘simply’ needed to know where I obtained the money to pay off my balance ($1800). Additionally, because I was now flagged as ‘in financial trouble’, once the hold was removed, they told me my credit limit would be cut in half. I cancelled the card – lesson learned.

What I love about this card is that it is such a eazy and practical way to receive your rewards. you don’t have wait forever to collect points till you have enough to do something with them. eg. air miles. you can buy your everyday household items with this card, it rocks!

Your CT website is not ready yet for the big league

I registered to pay Montreal city tax then the option came up I clicked on it several times with no success then I tried GAS bill . I’m looking for gas metro but GE is coming up !!!

i just got this card two months ago and a week ago (not even 3 months, let alone typical 6 months) they upped my limit by $1K which is fine. interest rate ive no idea what it is as i always pay the card in full before the statement due date. LOVE LOVE LOVE LOVE LOVE their customer service.

i used to love the walmart mastercard. well … lets just say i havent pulled that card out of the wallet since i got the canadian tire one. besides walmarts customer service for mastercard is BEYOND AND I MEAN BEYOND HORRIBLE.

have no loyalty to either brands, but just saying how it is. good for you canadian tire!